Part IV: Nobody Believes Your Forecast

I met a founder friend for coffee last week, an hour after he came out of an investor meeting. As he was telling me about it he opened his laptop and showed me the financial model he sent ahead of the pitch. It was, to be honest, beautiful. Five years planned, monthly columns, a dashboard tab with charts that updated themselves. He was really proud of the Year-5 revenue line, and the pride was earned - a lot of nights went into that number.

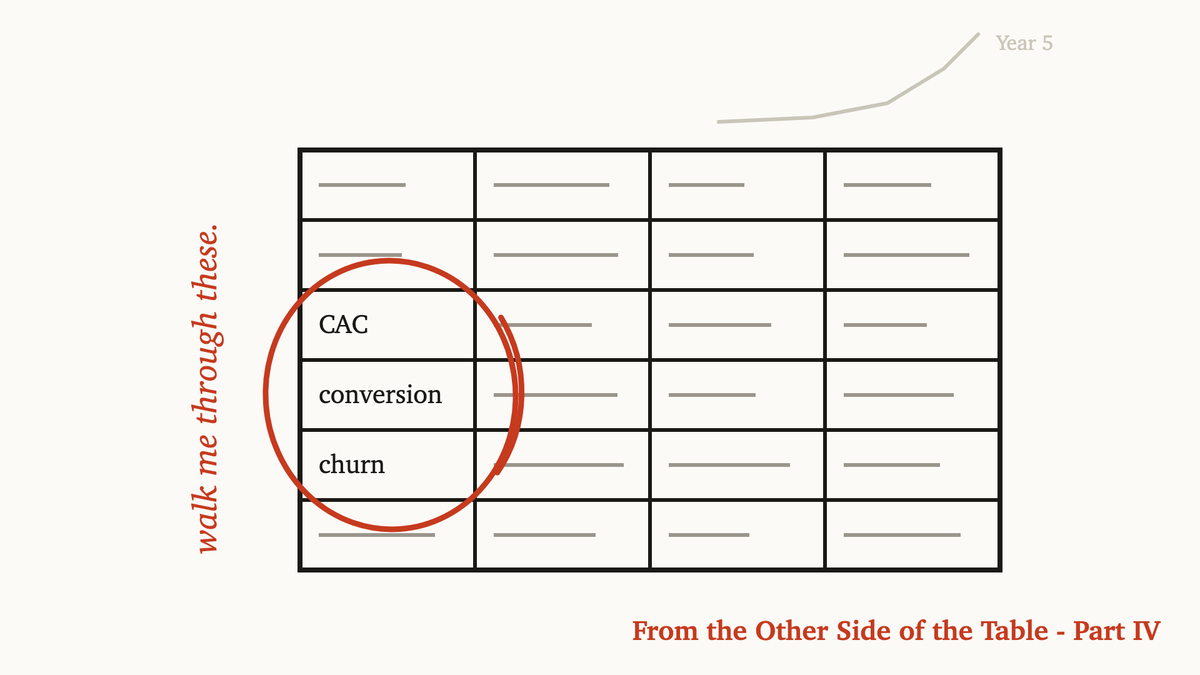

The meeting, as he told me, went differently. The investor scrolled past the dashboard, ignored the hockey stick, never reached Year 5. She stopped on three cells deep in the assumptions tab. Customer acquisition cost. Conversion. Churn. "Walk me through these."

The answer arrived by email a few days later: "We're going to pass for now." But my friend didn't need the email. He knew, walking out, that the meeting was decided in those ten minutes - on the part of the financial model he had spent the least time on, and couldn't defend.

I've reviewed a lot of these models. For six years I evaluated pet-tech startups from inside a corporate venture fund, and these days I read them from the advisor's chair - founders in pet, in human health, in music, plus the ones who just call for a second pair of eyes. The seat has changed; the conversation around the spreadsheet hasn't. And I've built these models myself as a founder - many of the mistakes below are mistakes I've made personally. When I wrote about what to actually send investors, I promised the financial model a piece of its own. This is that piece.

The model is about thinking, not forecasting

Here's the open secret: everyone in the room knows the projection is fiction. The investor knows it, you know it, the spreadsheet knows it. Nobody has ever funded a pre-seed company because Year 5 looked good, and nobody serious has ever believed a five-year forecast from a company with eight months of history.

The projection is the plan - worthless the day after you finish it. The planning is what the investor is actually reading. Do you know which three or four numbers drive your business? Can you explain where each assumption comes from? Did you model other go-to-market strategies, and what did that tell you? When an assumption gets challenged, do you have evidence, or just conviction? The model is the one document in your data room that can't hide behind good writing or flashy design. It's just your reasoning, in numbers.

And it matters more now than it did a few years ago. Venture capital has concentrated hard around AI, deal counts everywhere else have thinned, and the bar for what counts as proof keeps rising. If you're building outside AI - in pet, in health, in music, in any niche market - the question behind every meeting has gotten more brutal: can this founder be trusted with money? The model is where that question gets answered.

Fit the model to the stage

There are two common mistakes here. The first is the model that's too thin. A single tab. Revenue growing 20% a month because the template said so, costs an afterthought. It signals you haven't done the thinking, and the meeting adjusts accordingly.

The second is the model that's too much. I've been handed 29-tab models by pre-seed companies. Tax provisions. Full balance sheets. Collections delays modeled by customer segment - for a company with fewer than a dozen paying customers.

Founders think this signals rigor. From the other side of the table it signals the opposite: you don't yet know what matters. At pre-seed, three or four drivers decide whether your business works. A model that treats all two hundred inputs as equally important tells me you can't tell the difference. Worse, it tells me where your weeks went - and sometimes a CPA's or an economist's fees, too. That time and money belonged in conversations with customers. The overbuilt model is as much a red flag as the missing one.

The right size is the size of your actual uncertainty. Since that's abstract, here's the rough map I give founders when they ask.

Stage first. At pre-seed you're mostly pre-evidence, so the honest model is small: three years out, monthly for the first year, a tab or two, base case only. Its whole job is to answer five questions - how much you're raising, what you burn, how long it lasts, what milestones it buys, and when you'll need to raise again. At seed you have early data, and the model should show that you know it: five years with the later ones clearly directional, assumptions traceable to what you've measured, a real downside case next to the base one.

Then the drivers, which change with the business model. Subscription: churn, acquisition cost and how fast it pays back, conversion. Marketplace: take rate, repeat purchase, whether supply and demand actually stay on the platform. Consumer app: retention and free-to-paid conversion, with a real acquisition cost behind them. Hardware: gross margin after everything lands - freight, duties, returns - and the cash tied up in inventory, which kills more hardware companies than weak demand does. Three or four numbers each time. Different numbers, same discipline: an investor should be able to absorb the whole thing in twenty minutes and know exactly what you believe.

Assumptions you can defend

Which brings us to the part that actually decides things: those three or four numbers. The entire model is downstream of what you assumed about each.

"Defensible" doesn't mean impressive. It means three things: you know exactly what each number assumes, you tied it to the least flattering metric available, and when someone pushes, you can stand behind it.

Two patterns show up constantly. The first is the flattering version of a true number. A deck shows customer acquisition at $14. True, technically - as a blended figure, with an early organic bump doing most of the work. The paid channels, the ones that would actually have to carry the growth the model promises, acquire at around $47. Both numbers are in the model; only one made the slide. An investor finds this in minutes, and once found, it re-prices everything else you've claimed - not because $47 is a bad number, but because you chose to show the other one.

The second is the formula nobody interrogated. A revenue projection driven by app installs. But installs don't pay - active users pay - and the gap between the two compounds to a factor of three by Year 2. One cell, tied to the wrong metric, quietly overstating revenue threefold. Not fraud, not even really a lie. Just an assumption sitting under the entire model that nobody had questioned.

Is your churn monthly or yearly? Does "revenue" mean billed or collected? The list is long; the art is knowing which of these questions matter for your business, because in the actual meeting there's no second pass.

Back to my friend

The pass hurt less than the part he already knew: the model questions were where the meeting turned, and he had prepared for everything except them. The Year-5 number, the precision of the curve, the conditional formatting - everything he polished sits near the bottom of the investor's list. (His own planning is a different story; the discipline is worth it for him. It just doesn't move the meeting.)

So we've scheduled a working session to do it in the right order this time: find the three or four drivers that actually carry his business, walk each assumption back to its most honest source, debug the formulas underneath, and make sure that when someone leans on the model, it doesn't break. The Year-5 number will barely change. What the model says about him will.

That's the reframe I'd offer any founder about to hit send on a spreadsheet: the model isn't a prediction you're asking investors to believe. It's the clearest view they'll get of how you think. In the next part, the last in this series, I'll turn that lens around: the questions an evaluator actually asks, handed over, so you can run them on yourself before someone else does.

I help founders navigate strategy and funding decisions when the path isn't clear. If you're there, let's talk.

If this was useful, I write one of these most weeks.

Subscribe on LinkedIn